Synopsis – looking at the changing landscape on electric vehicles with special insights from Thailand.

I. BACKGROUND

Reading the news in the last quarter of 2021, you would not miss the media attention to Conference of Parties (COP 26) 2021, the gathering of signatories of the UN Framework on Climate Change, which again is stirring up concerns about decarbonization, as post Covid-19 crisis countries around the world are striving to rebuild economies sustainably.

In the South East Asia Climate Outlook Survey 2021 carried out by ISEAS – Yusof Ishak Institute Singapore which covered 610 respondents from all 10 ASEAN nations, there was strong consensus on the potential of tapping the renewable energy sector emerging across the region. When asked how ASEAN governments would collectively combat climate change, the top most popular option was investing in renewable energy (51.8%).

One sector clearly forging ahead to drive conversion to alternatives is the automotive industry and the electrification of vehicles. The automotive industry is set to be heavily affected by the new sustainability and environmental policy changes. Combined with disruptive technology trends such as autonomous driving, vehicle connectivity and new industry players with data and AI expertise, dramatic upsets are foreseeable.

To solve climate change, transport has to go green and electric.

Of course the question is how truly green are EVs? A recent study by Argonne National Labs published in 2018 (The Impacts of Electrification of Light Duty Vehicles in the United States 2010 – 2017) reached some interesting conclusions. The study found use of electrified vehicles in the US in that 8 years period (2010 – 2017), reduced US gasoline consumption by 600 million gallons and net carbon emissions by 2.6 million metric tons. This reduction was achieved with US penetration of hybrid and fully electric vehicles at less than 1% of total vehicles sold in that period. Although critics may argue the assumptions are subject to challenge, the facts appear to support the favorable impact of EVs.

II. THAILAND

National Policies

Thailand’s automotive industry is well developed and has been established over several decades. Today, Thailand has become the largest automotive producer in Southeast and surges ahead of Indonesia, Malaysia, the Philippines and Vietnam. The automotive industry contributed about 10 -12% to Thailand’s GDP. This success has earned Thailand the title of ‘Automotive Hub of Asia’.

While Thailand has been successful in producing the conventional Internal Combustion Engine (ICE) vehicles, the push for reducing emission in global transportation has led to the growth and demand for EV production. What has Thailand moved towards in preparation for EV transformation?

As far back as 2017, the Thailand Board of Investment (BOI) had already offered investors a package combining both highly competitive investment tax and non-tax incentives. In early 2020, the government established the National Electric Vehicle Policy Committee (NEVPC) to oversee the EV roadmap for the country with the target of promoting the production and use of electric cars. The ambition was to have 30% of the total car production as EVs by 2030. Towards this end, many key national policies on promoting and accelerating EVs transformation have been designed and implemented.

- Investment Tax Incentives

After the first BOI incentives package of the expired in 2018, new tax incentive schemes were launched including tax holidays for qualified EV projects and businesses in the EV supply chain, in particular the EV battery industry. These incentive schemes were expanded to include passenger cars, buses, trucks, motorcycles, ships, and bicycles. The table below highlights the advantages based on type of vehicle;

The BOI took a larger industry perspective and also rolled out CIT exemption to the EV part and equipment manufacturers such as voltage harnesses, reduction gear, battery cooling systems, and regenerative braking systems. Businesses in these four categories are eligible to receive up to 8 years of CIT exemption.

Further to promote and encourage ”made in Thailand” electric vehicle parts which are key and/or necessary for production of EVs, the BOI has granted a 90% reduction in import duties for raw materials used in the production of batteries that are not available locally for a period of two years from 4 November 2020 to 4 November 2022. EVs plants set up under Eastern Economic Corridor (EEC) investment campaign enjoy all these additional incentives.

As of September 2021, the BOI has approved a total of 31 projects with investments of over 86,700 million Baht.

- General Tax Scheme

There are four different types of tax schemes currently available in Thailand including the import duty, excise tax, interior tax and value-added tax. EVs import duty rate in Thailand varies depending on bilateral agreements made with other countries. For example, Thailand has an existing Japan–Thailand Economic Partnership Agreement (JTEPA) where the import duty is subject to 20%, while the EVs importation from China will enjoy the best benefit of 0% import duty due to the Free-Trade Agreements (FTAs) between Thailand and China. EVs imported from South Korea are subject to 40% import duty and 80% import duty if those are imported from Europe.

The current Thai excise tax structure was established in 2016 to favour the EV industry where the excise tax for EV cars produced in Thailand was reduced from 10% to 8%, and 2% in a bold move in 2020, the BOI reduced excise tax to 0% for a period of two years to accelerate the industry transformation for EVs in Thailand.

The interior tax is currently at the rate of 10% calculated from the excise tax and the 7% for the value-added tax, which is calculated from the sum of the CIF, import duties, excise tax and interior tax.

- Electricity Cost for EVs charging

Developing an ecosystem to encourage the use of EVs is fundamental to this transformation and having charging stations and outlets for EVs is necessary to persuade consumers to switch to purchase and use of EVs.

As of June 11, 2021, Thailand has a total of 664 electric charging stations with a total of 2,224 chargers for both normal and fast charging. Most of these are located in Bangkok and its surrounding areas. In the same year the government approved a standard cost of electricity for all EV charging stations at a relatively low price of 2.63 Baht/kWh if off-peak and 4.3 Baht/kWh for peak tariff. With such competitive pricing the number of charging stations and outlets will likely increase; correspondingly it is expected that the number of service providers will increase and competition heat up.

III. EV USAGE IN THAILAND

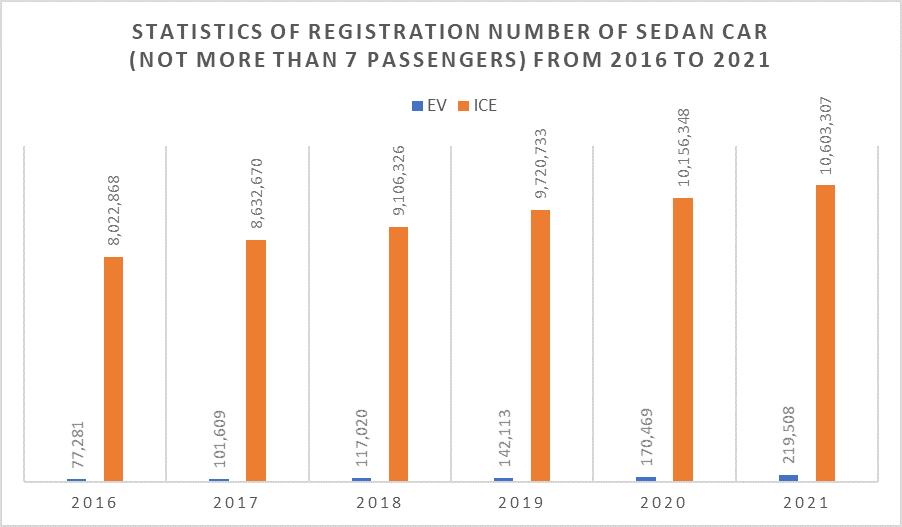

According to the data from the Department of Land Transportation of Thailand, the number of all types of EVs registration from 2016 to 2021 (as of November) has more than doubled by 200%, from 79,383 units to 235,885 units.

Analysing the statistics of a sedan car (see table above) the proportion of EVs registered as against ICEs is rapidly increasing from 0.9% in 2016 to about 2% in 2021. Comparing with the rapid growth of EVs globally, we expect a similar trend as EVs become more popular in Thailand.

IV. GLOBAL EV AND RELATED TECH TRENDS

Clearly leading the charge in Asia and globally is China, the largest auto market with a competitive and comprehensive EV supply chain. Forecasts predict the EV sales in China will hit 18 million come 2030. The number is only 10% today. Globally the EVs have less than 1% market penetration in 2021, but demand is expected to rise, just as we have seen in the Thai study above.

In China, the motivation was twofold – not only to deal with emerging issues and maintain its global leadership position in the automotive space but also to control some of the world’s worst air pollution in its major cities, to seek a solution through electric vehicles. A coordinated Chinese government effort resulted in increased EV investment by existing and new vehicle OEMs and stimulated market demand for electric vehicles. Again like Thailand, the Chinese authorities also encouraged consumers to select EV models through tax incentives and wide availability of charging stations in major metropolitan areas.

It is of note that consistent with the assessment by Thailand and its policy makers, a focus on key component manufacture will influence the growth of the industry – of the various parts, of greatest importance is the battery for EVs. Why focus on battery technology? Studies show that batteries and its related materials constitutes 60% pf EV component costs.

Technology relating to batteries and battery powered electric vehicles (BEV) is not as new as many think and have been around since the 90’s. Efforts by General Motors and Nissan resulted in early roll outs of their proprietary vehicles which had commercially viable battery powered passenger cars. We also saw new cars using both fully electric and hybrid systems. The market also saw Toyota’s Prius which had a hybrid electric/internal combustion powertrain, became the global market leader for “green transportation. Nevertheless the take up was still relatively slow until the introduction of the Tesla Model S in the US market which included improvements to battery and electric powertrain technology in a sleek design. When this captured the attention of both investors and the vehicle buying public, it was a breakthrough.

Today Europe is also more actively engaged with a focus on green lifestyles. We see a developing active market for new EV models from a growing number of local vehicle producers. We see this clearly captured in the table from ICCT below.

V. INTELLECTUAL PROPERTY AND INNOVATION

With this data, what then should OEM players, manufactures in the supply chain, investors and the automotive players be looking out for? What IP strategies are needed to be competitive in the EV space, if you have the deep pockets or the technology to continue in the space?

Some would argue that the focus should be on the new elements of the EV ecosystem and work with IP professionals to understand these technical and market changes well so as to support or create new solutions that are owned and protected.

With immense competition in the EV and automotive space and the heavy investment required, aside from tax and other incentives, central to ownership of all the innovation and technology is the IP and in particular patents that ensure innovation is properly captured and return of investment assured.

As mentioned above greener technology for EVs relate to sources for the electricity. The 2022 Toyota Mirai hydrogen fuel tanks generating electricity with zero emission. At the core is the Mirai hydrogen fuel tank and the fuel cell stack that allows a chemical reaction involving the air and hydrogen creating electricity, with only water as by-product.

The Mirai has multiple portfolios of patents covering the hydrogen fuel tanks, battery and system it uses within the EV. It declares the same in its marketing material as recognition it has IP arsenal in this technology.

If you make, use, distribute, offer for sale, import or supply products and services, (all patent exploitation rights), you will need to recognise also as much as you need to own the IP from your innovation, you need to manage the growing IP risks of venturing into emerging areas. Planning for such risks includes defining, anticipating and preparing to address these questions, whether in the strength of your own rights or recognising the strengths of others in the space. Building your own IP portfolio is a means to respond to IP risk and the effectiveness of the measure bears repeating. As this takes time it is not an action you can mount overnight unless you have extremely deep pockets and are able to go on an acquisition spree as how LinkedIn responded in 2017/2018 when it realised it needed to charge up its portfolio and profile urgently and ended up buying over 900 patents for a significant sum.

Efficient operation of these new energy systems will require software-based control systems to not only regulate vehicle powertrain operation, but also to interface with vehicle charging and hydrogen storage infrastructure. Robust IP protection for this software is key to maintaining competitive advantages for firms in a competitive global marketplace.

- Tech landscape

To illustrate the point, a simple patent landscape search of EV batteries will show the terrain and can inform R & D strategy. A more complete study can facilitate careful analysis so that a quality and relevant IP portfolio can be developed or even acquired.

An example of understanding relevant tech includes looking at reducing the cost of the battery pack such as Lithium-Ion battery systems as these are the overwhelming favourite technology of choice for EV systems – what developments are there that R&D teams need to be aware of so as not to reinvent the wheel?

Similarly speed in charging is recognised as one key development needed in the EV space and according to encourage adoption by time constrained drivers, fast charging is a great incentive but data is showing that continually using high-powered, fast-charging points can decrease the life of EV car batteries. Engineers from the University of California, Riverside say that commercial fast-charging stations subject EV car batteries to high temperatures and resistance which can cause cells to crack, leak, and lose storage capacity. According to the researchers, the standard process effectively killed the batteries after just 25 charging cycles. Another aspect is recognising if using the industry standard charging process, battery capacity was reduced by as much as 40% after 40 charge cycles but using the internal resistance-based method battery capacity was only reduced by about 20% by the 40th charge cycle. It should be noted that an EV car battery is considered end-of-life when it holds less than 80% of its original total capacity.

Understanding such data helps in focus when inventing and R&D. If your invention overcomes the above known constraints and uses unexplored technical solutions to solve these problems, you are likely to have a patentable invention.

- Access to third party IP

There are private entities that contribute in encouraging innovation in the EV space for greater adoption and economic viability for all. Other organisations have safety, security or interoperability as objectives, particularly associations that are established by members in the sector. In both cases, access to IP is given.

It may be useful to know that vehicle OEMs have been making certain IP available at low or no charge to facilitate adoption of electrified powertrains in cars and light trucks. For example Toyota offer for free use of hybrid car patents through 2030. Tesla applies its open-source philosophy to its patents see https://www.tesla.com/blog/all-our-patent-are-belong-you

The Society of Automotive Engineers (SAE) operates in the US and other countries. SAE and other automotive engineering groups work together to establish standards that promote vehicle safety and interoperability in world markets. Its members who are patent holders for technologies are expected to abide by SAE policy relating to proprietary technology contained in the Technical Standards Board Governance Policy 15th Revision – October 2017.

It is instructive to read the relevant provision to understand the philosophy behind SAE’s thinking

1.13.3 Patents

It has been traditionally the position of SAE to avoid the use of patented technology in Technical Reports where the principal objective is conformance to the Technical Report as defined by the SAE Technical Standards Board.

However, with the advent of more complex technologies, it is not always possible to provide Technical Reports that meet today’s needs without incorporating technologies that are patented. It has become difficult, if not impossible, to develop standards that do not take advantage of or otherwise incorporate the use of products, systems or process that implementation would necessarily infringe a claim of such a patent. Accordingly, SAE Technical Reports may include the known use of patent(s), including patent applications, if there is in the opinion of the committee developing the Technical Report technical justification and provided that SAE receive assurance from the patent holder that it will license applicants under reasonable terms and conditions for the purpose of implementing the standard. This assurance shall be provided without coercion and prior to the approval of the standard or reaffirmation when a patent becomes known after the initial approval of the standard. This assurance shall be a letter that is in the form of either:

A general disclaimer to the effect that the patentee will not enforce any of its present or future patent(s) whose claims would be necessarily infringed by implementation of the proposed SAE Technical Report against any person or entity implementing the mandatory provisions of the Technical Report to effect compliance or;

A statement that a license will be made available to all applicants without compensation or under reasonable rates, with reasonable terms and conditions that are demonstrably free of any unfair discrimination.

The above underscores the importance that to be recognised as a serious player or “gain a seat at the table”, it helps to have IP to contribute. Having said that, being prepared to licence on fair and reasonable terms will be necessary for the purposes of being included in a standard.

VI. SUMMARY AND CONCLUDING THOUGHTS

This is a fascinating area that is dynamic and exciting. Clearly we can surmise from this article there are key movers and enablers that are catalyzing the changes and moving us towards widespread adoption globally. These include government policies and incentives such as those seen in Thailand and China where orchestrated efforts are pushing the national agenda effectively. China has an advantage and correspondingly the greatest opportunity as it already holds 60% market share of the EV global market share, set to hit US$356 billion within the next decade. With Thailand aiming for 30% of total automotive production to be EVs by 2030, we anticipate more sweeteners and policies to continue to be rolled out there.

We are also seeing the ecosystem developing with battery EV systems, although still more expensive, making important progress towards being cost effective technologies to adopt. Also access to third party IP to build on, is ensuring greater safety, interoperability and correspondingly adoption as consumers gain more confidence in EVs.

Significant opportunity for providers of vehicle, automotive systems and charging infrastructure will come from these new elements of the EV ecosystem and investors recognizing these emerging trends, particularly with new players like Tesla, Nio and competition coming from unexpected quarters, including universities and start-ups.

We foresee that IP in EVs will continue to pay an important role for its owners and create opportunities for IP deals – whether due to acquisition of much needed disruptive but key innovations covered by patents, IP supported market position, licensing or IP driven collaborations. Understanding and reacting to these changes and working with a strong team of IP experts supportive of building robust IP portfolios or designing such transactions with make a difference to those left standing in this competitive industry in the mid to longer term. Much remains to be invented and perfected in this competitive market and your firms can be part of this exciting future.

We acknowledge the kind contribution of John Carney, Managing Director, China IP Exchange, and LLC for his review thoughts and insights in the writing of this article.

If you would like to have further information on this write-up, please contact:

Audrey Yap (Ms.)

Regional Managing Partner

D (65) 6358 2865

F (65) 6358 2864

audrey@yusarn.com

Kamonphan Minjoy (Ms.)

Director, Patents and Trade Marks

Yusarn Audrey Thailand

163 Thai Samut Building

14th Floor, Unit 14H

Surawongse Road, Suriyawongse, Bangrak, Bangkok 10500, Thailand

T: (66) 2-234-1585-88

F: (66)-2-234-1589

minjoy.th@yusarn.com